By Canooq Editorial on May 25, 2026

Estimated reading time: 8 minutes

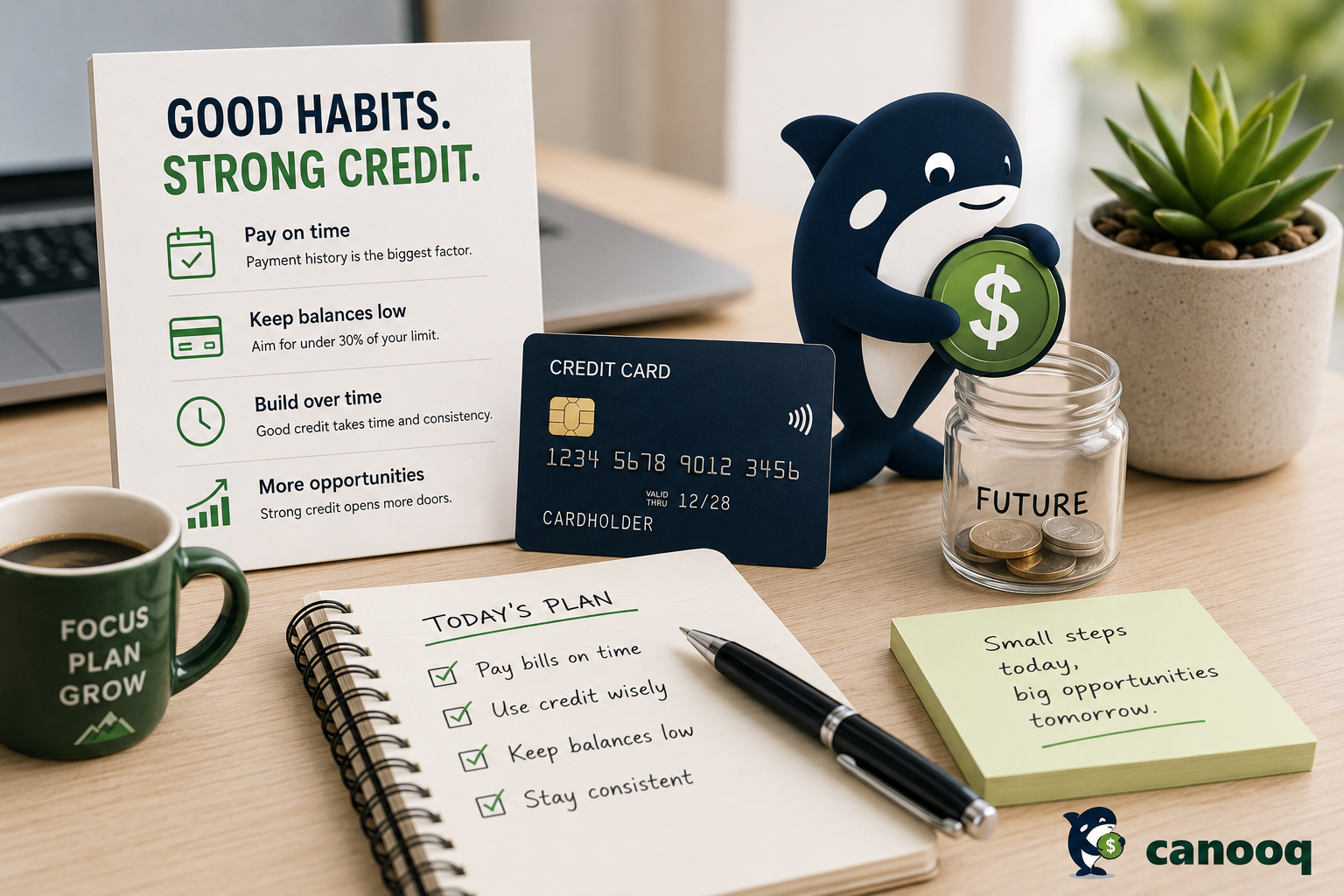

How to Build Credit in Canada From Scratch (Without Going Into Debt)

A practical guide to building a strong credit score from zero, avoiding common mistakes, and unlocking better financial opportunities.

In this guide

A practical guide to building a strong credit score from zero, avoiding common mistakes, and unlocking better financial opportunities.

Why Your Credit Score Matters in Canada

Your credit score quietly affects a huge part of your life in Canada.

See also

Cashback Apps: What to Check Before Signing UpRead nextFEATURED

Ergonomic Mesh Office Chair

A comfortable adjustable chair with lumbar support that's perfect for long workdays.

★FEATURED

Interactive Brokers

Invest globally with low fees and professional tools built for serious investors.

Welcome Bonus15 minBonus

Up to USD 1,000 in IBKR stock

Conditions

Open an account through the referral link

When paid

Shares are awarded after qualifying deposits

Access

Stocks ETFs options and more

Welcome Bonus

Up to $1,000

A strong score can help you:

- Get approved for apartments

- Qualify for better mortgage rates

- Access premium credit cards

- Finance a car more easily

- Avoid large security deposits

- Improve approval odds for phone plans or utilities

If you are new to Canada, a student, or simply starting from zero, the good news is that building credit is actually very simple when you understand the rules.

See also

Referral Codes Without the AwkwardnessHow Canadians use referral bonuses strategically without annoying friends or breaking trust.Read nextWhat Is Considered a Good Credit Score?

In Canada, credit scores usually range from 300 to 900.

Here is the general breakdown:

- 300–559 → Poor

- 560–659 → Fair

- 660–724 → Good

- 725–759 → Very good

- 760+ → Excellent

For most people, reaching around 700 already unlocks most useful financial products.

The goal is not perfection. The goal is consistency.

The Fastest Way to Build Credit

The easiest strategy is surprisingly boring:

- Get a beginner credit card

- Use it for small normal purchases

- Pay it in full every month

- Repeat for 6–12 months

That is genuinely enough.

You do not need to carry debt or pay interest to build credit.

The 30% Rule (That People Misunderstand)

You may hear that you should “stay below 30% utilization.”

This simply means:

- If your card limit is $1,000

- Try not to report more than about $300 used

High utilization can temporarily lower your score even if you pay on time.

A simple trick:

- Use the card normally

- Pay part of it before the statement date

This keeps your reported balance low.

The Biggest Beginner Mistakes

Missing a Payment

Even one missed payment can stay on your report for years.

Set up:

- Auto-pay

- Calendar reminders

- Minimum payment protection

Applying for Too Many Cards

Every hard inquiry slightly impacts your score.

Do not apply to five cards in the same week.

Closing Old Cards

Your oldest accounts help your credit history length.

If a no-fee card is old, keeping it open is usually beneficial.

Best First Credit Cards in Canada

For beginners, the ideal card has:

- No annual fee

- Simple approval requirements

- Cashback rewards

- A reasonable starting limit

FEATURED

Wealthsimple Cash

Popular beginner-friendly account with cashback and occasional welcome offers for Canadians starting their financial setup.

FEATURED

Neo Financial Mastercard

Often easier approval for newcomers and students with strong cashback categories.

How Long Does It Take to Build Good Credit?

Approximate timeline:

- 1–3 months → credit file appears

- 6 months → first meaningful score

- 12 months → solid beginner profile

- 24+ months → strong long-term history

Consistency matters far more than intensity.

Extra Ways to Improve Your Credit

Keep Old Accounts Open

Age of accounts helps.

Increase Your Credit Limit Slowly

A higher limit lowers utilization percentage.

Diversify Over Time

Eventually having:

- A credit card

- A phone plan

- Maybe a car loan or line of credit

…creates a stronger profile.

Do not rush this step early.

Should You Pay Interest to Build Credit?

No.

This is one of the most common myths in personal finance.

Banks report:

- payment history

- utilization

- account age

—not whether you paid interest voluntarily.

If possible, pay your balance in full every month.

What Newcomers to Canada Should Do First

If you recently moved to Canada:

- Open a bank account

- Apply for a starter credit card

- Put one recurring payment on it

- Enable auto-pay immediately

Phone bills and secured cards can also help create your first credit history.

See also

Cashback Apps: What to Check Before Signing UpRead nextFinal Thoughts

Building credit in Canada is less about complicated strategies and more about avoiding mistakes.

The people with the strongest scores usually do the same simple things for years:

- Pay on time

- Keep utilization low

- Avoid unnecessary debt

- Keep accounts open

Start early, stay consistent, and let time do the heavy lifting.

Read more about saving:

See also