Smith Manoeuvre Canada: How It Works, Risks, and What Can Go Wrong

June 12, 2026

A detailed Canadian guide to the Smith Manoeuvre, including how the mortgage-to-investment debt conversion works, why interest may be deductible, what can fail, and the major risks.

MORTGAGE + INVESTING

The Smith Manoeuvre is borrowing to invest, not free money.

It can gradually convert non-deductible mortgage debt into potentially deductible investment debt, but only when the household can handle leverage, clean records, taxes, and market risk.

- A normal mortgage is usually personal debt, so the interest is not deductible.

- The strategy borrows against home equity to invest in a taxable account.

- The interest may be deductible only when the borrowed money is used and documented properly.

Check the cash-flow pressure first

Use this as education, then confirm the tax and lending details with qualified professionals.

What's on this page

The Smith Manoeuvre gradually converts personal mortgage debt into investment debt by using readvanceable home equity to invest in a taxable account. It can create deductible interest, but it also adds leverage, tax complexity, rate risk, market risk, and record-keeping pressure.

The Smith Manoeuvre is a Canadian borrowing-to-invest strategy built around one tax difference: interest on money borrowed for personal use is generally not deductible, while interest on money borrowed to earn investment income may be deductible when the rules are met. A home mortgage is usually personal debt. A properly traced investment loan can be different. The strategy tries to move debt from the first bucket to the second bucket over time.

The core idea

Most Canadian homeowners pay mortgage interest with after-tax dollars and cannot deduct it. If they borrow money and use that borrowed money to buy investments in a taxable account with a reasonable expectation of earning income, the interest on that borrowing may be deductible. The Smith Manoeuvre uses a readvanceable mortgage or linked home-equity line of credit to make that conversion gradual.

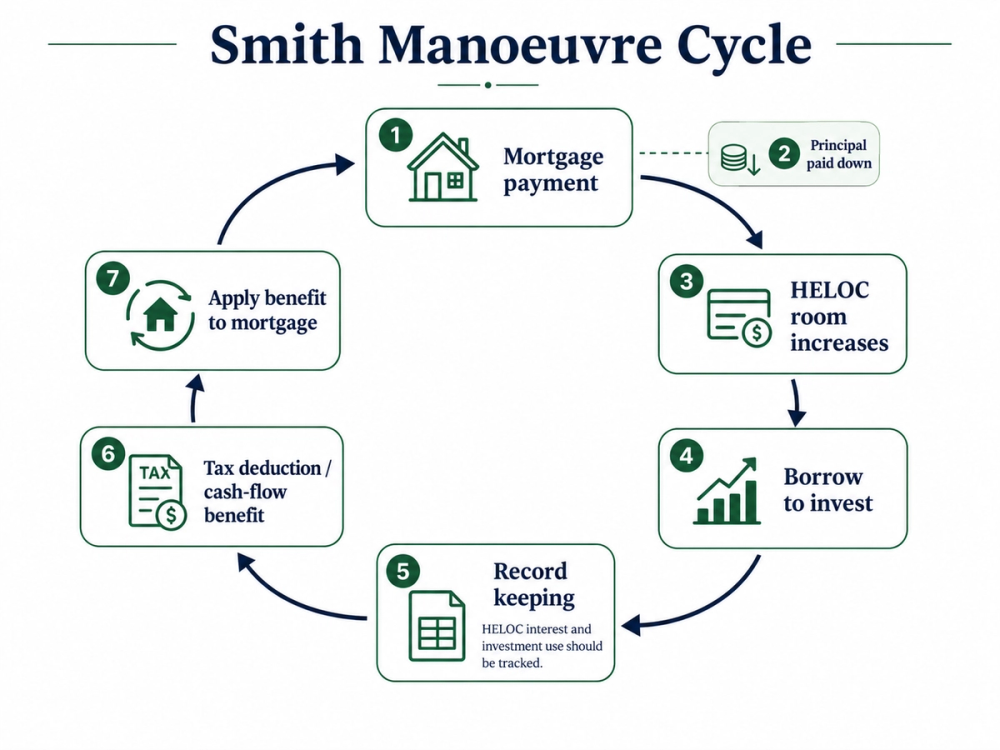

There are three separate things happening at once:

- Mortgage principal goes down. Each regular mortgage payment includes some principal. That reduces the personal mortgage debt.

- Borrowing room goes up. With a readvanceable setup, some paid-down principal can become available again as secured credit.

- Investment debt grows. You borrow the newly available credit and invest it in a taxable account, while tracking the interest separately.

The account setup

The clean version usually needs a readvanceable mortgage, a separate home-equity credit line or sub-account, a non-registered investment account, and disciplined banking records. The credit line is secured by the home. The investment account is taxable. The records must show that borrowed money went to investments, not groceries, renovations, vacations, tuition, or a mixed chequing account.

Common moving parts

Names vary by lender and brokerage, but the functions are usually similar.

| Part | What it does | Why it matters |

|---|---|---|

| Mortgage | The original home loan used to buy the property. | This interest is normally personal and not deductible. |

| Readvanceable credit line | Credit room increases as mortgage principal is paid down. | This creates the borrowing source for the strategy. |

| Taxable investment account | The account where borrowed money is invested. | The account must be separate enough to trace borrowed funds clearly. |

| Interest records | Statements showing interest charged on the investment borrowing. | These support any interest deduction claimed on the tax return. |

Step-by-step: how the cycle works

- Make the regular mortgage payment. Part of the payment pays interest and part pays principal. The principal portion reduces personal mortgage debt.

- New credit room becomes available. If the mortgage is readvanceable, the principal paid down can increase the linked credit line or investment loan room.

- Borrow only from the investment credit line. The withdrawal should come from the dedicated borrowing account, not a mixed-purpose personal line.

- Move the borrowed money directly to the taxable investment account. A clean transfer path makes it easier to show what the money was used for.

- Buy investments intended to earn income. The tax logic depends on the use of borrowed money. Many investors use diversified funds or stocks with an income expectation, but the exact investment choice needs its own risk review.

- Track the interest charged on the borrowed money. The interest may be deductible when the legal tests are met and the records support it.

- Repeat as the mortgage amortizes. Over years, the personal mortgage balance may shrink while the investment loan grows. Total debt may not fall much at first; its purpose changes.

A simple example

Imagine a homeowner makes a $2,500 mortgage payment. Suppose $1,200 of that payment is principal. In a readvanceable structure, roughly $1,200 of new credit room might become available. The homeowner borrows $1,200 from the dedicated credit line and invests it in a taxable account. The original mortgage is $1,200 lower. The investment loan is $1,200 higher. The household still owes money, but the new $1,200 debt has a different purpose.

That is the conversion. It is not a bonus, rebate, or guaranteed return. The homeowner has deliberately borrowed against the home to own investments. The possible benefit comes from long-term investment growth, investment income, and deductible interest. The possible damage comes from market losses, higher rates, tax mistakes, and weak cash flow.

Why the interest can be deductible

The important concept is use of borrowed money. In Canada, deductibility generally depends on what the borrowed funds are used for, not simply what secures the loan. A loan secured by your home is not automatically personal or deductible. If the borrowed money is used for personal spending, the interest is personal. If the borrowed money is used to earn income from property or a business, the interest may qualify.

- Security is not the point. The home may secure the line of credit, but the tax question is the use of the borrowed funds.

- Tracing is the proof. You need to show the path from borrowing to eligible investment use.

- The income expectation matters. The investment should have a reasonable expectation of producing income, not only a hope of a tax-free-looking capital gain.

- Tax advice matters. Deductibility can depend on details: investment type, account flow, repayments, refinances, distributions, return of capital, and record quality.

What 'capitalizing interest' means

Some versions of the strategy borrow additional money to pay the interest on the investment loan. That is called capitalizing interest. It can keep monthly cash flow easier because the household is not paying investment-loan interest out of salary, but it also makes the investment debt grow faster. This is more aggressive. It relies on lender permission, clean records, and the ability to tolerate a larger debt balance.

What makes the strategy work

- Positive long-term investment outcome. The investments need to do well enough over time to justify the borrowing cost, taxes, volatility, and complexity.

- Borrowing cost control. If the credit-line rate rises sharply, the hurdle rate for the strategy rises too.

- Stable household cash flow. Mortgage payments, investment-loan interest, tax instalments, and emergencies all need room.

- Clean separation. Personal borrowing and investment borrowing should not be mixed.

- Long time horizon. Short time horizons make market drops and rate spikes more dangerous.

- Behavioural discipline. The strategy can fail because someone panics, spends the credit line, chases risky investments, or stops tracking details.

What can fail

The Smith Manoeuvre can break in several ordinary ways. None require a dramatic crisis. A few small mistakes repeated over years can be enough.

- The investments fall. Borrowing magnifies exposure. If the portfolio drops 30%, the loan does not drop with it.

- Interest rates rise. Home-equity credit lines often have variable rates. Higher rates increase carrying costs and reduce the chance the strategy adds value.

- The lender changes limits. Credit limits, advance rules, appraisals, renewals, and underwriting can change. Do not assume access to credit is permanent.

- Cash flow gets tight. Job loss, parental leave, illness, repairs, or higher mortgage payments can force selling investments at a bad time.

- Records get messy. If borrowed money is mixed with personal spending, the deductible portion can become hard to support.

- Tax rules or interpretation change. A strategy that depends on tax treatment needs monitoring.

- The plan becomes too concentrated. Using home equity to buy risky or concentrated investments stacks home risk and market risk together.

The record-keeping rules of thumb

- Use a separate credit line or sub-account for investment borrowing where possible.

- Do not use the investment credit line for renovations, cars, vacations, tuition, household bills, or emergency spending.

- Transfer borrowed funds directly to the taxable investment account.

- Keep monthly credit-line statements, brokerage statements, trade confirmations, tax slips, and a simple spreadsheet showing each borrow-and-invest cycle.

- Track any investment distributions carefully, especially return of capital, because it can affect interest tracing.

- Keep tax returns and supporting documents for the period required by CRA, and longer if the loan remains active.

Who might consider it

- A homeowner with strong equity, stable income, and a long investing horizon.

- Someone who already understands taxable investing and can handle portfolio volatility.

- A household with emergency savings and no high-interest consumer debt.

- Someone willing to pay for tax and mortgage advice before claiming deductions.

- A person who can keep records even when life is busy.

Who should probably avoid it

- Anyone whose mortgage already feels uncomfortable.

- Anyone using the credit line to fill monthly budget gaps.

- Anyone who would sell during a market crash just to stop feeling anxious.

- Anyone who wants a strategy that works only if tax savings arrive exactly as expected.

- Anyone with unstable income, weak emergency savings, or expensive consumer debt.

- Anyone who dislikes paperwork, tax details, or ongoing monitoring.

Questions to ask before starting

- Could I handle higher mortgage payments and higher credit-line interest at the same time?

- Would I still hold the investments if they fell 25% while the loan stayed the same?

- Can I explain exactly where every borrowed dollar went?

- Do I understand the tax treatment of the investments I plan to buy?

- Do I have a written exit plan if rates rise, income drops, or I need to sell the home?

- Have I confirmed the plan with a mortgage professional and a tax professional?

Stress-test the plan first

The strategy should be tested against boring but realistic numbers before any borrowing starts.

Bottom line

The Smith Manoeuvre is a debt-conversion and leverage strategy. It can make sense for a small group of homeowners who are financially stable, organized, tax-aware, and comfortable investing through volatility. It is not a hack for making a mortgage cheap. It is a long-term plan that uses home equity to invest, with the home, the tax return, the investment account, and the household budget all connected.

The easiest way to misunderstand it is to focus only on the tax deduction. The deduction is one part of the equation. The full equation includes investment returns, borrowing costs, tax rules, record keeping, lender behaviour, market declines, personal stress, and the possibility that simple mortgage repayment would have been the better risk-adjusted choice.

Related articles:

Page details

Author: Canooq Editorial

Updated: June 12, 2026

Cite this page: Canooq.ca, Smith Manoeuvre Canada: How It Works, Risks, and What Can Go Wrong, https://canooq.ca/blog/smith-manoeuvre-rrsp-manoeuvre-canada

Canooq content is educational and may include affiliate or referral links. It is not financial, tax, legal, immigration, employment, mortgage, real estate, or healthcare advice. Verify official sources and provider terms before acting.