TFSA vs RRSP vs FHSA: Which Account Should You Use First?

By Canooq Editorial

June 3, 2026

A practical Canadian guide to choosing TFSA, RRSP, or FHSA first based on home-buying plans, income, flexibility, retirement goals, newcomer status, family benefits, and self-employment.

ACCOUNT ORDER

Match the account to the life goal.

FHSA is strongest for eligible first-home buyers, TFSA is strongest for flexibility, and RRSP is strongest for tax-deferral retirement planning.

- Use FHSA first if you qualify and a first home is a real goal.

- Use TFSA when you need flexibility, emergency savings, or uncertain timing.

- Use RRSP when there is an employer match, high income, or a retirement tax strategy.

Run the numbers

Use the decision order, then confirm your own room and eligibility with CRA.

What's on this page

FHSA usually comes first for eligible first-time buyers. TFSA is the flexible account for emergency savings and uncertain goals. RRSP is strongest for employer matches, higher income, and retirement tax planning.

TFSA, RRSP, and FHSA are all registered accounts, but they are not interchangeable. The right first choice depends on whether you want a home, how high your income is, how much flexibility you need, and whether retirement saving is the main goal.

What each account is

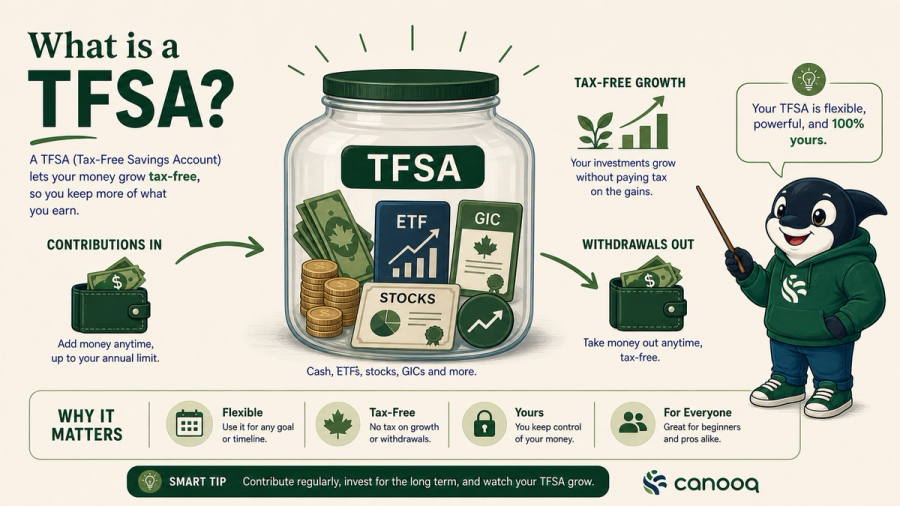

TFSA stands for Tax-Free Savings Account. You contribute after-tax money. You do not get a deduction when you contribute, but eligible growth and withdrawals are generally tax-free. You can withdraw money for almost any reason, and the withdrawn amount is generally added back to your TFSA room the next calendar year. Despite the word savings, a TFSA can hold cash, GICs, ETFs, stocks, and other eligible investments.

RRSP stands for Registered Retirement Savings Plan. You contribute pre-tax-style money in the sense that contributions can reduce taxable income. The refund is not magic income; it is tax deferral. The account is strongest when you deduct at a higher tax rate now and withdraw later at a lower tax rate. Withdrawals are generally taxable, which is why RRSP money is usually retirement money.

FHSA stands for First Home Savings Account. It is designed for eligible first-time home buyers. Contributions are generally deductible like an RRSP, and qualifying withdrawals for a first home can be tax-free like a TFSA. That combination is why the FHSA is powerful when a first home is a real goal.

The tax logic in plain English

- TFSA: no deduction today, but tax-free growth and flexible tax-free withdrawals later. Great when flexibility matters.

- RRSP: deduction today, taxable withdrawal later. Great when your tax rate today is meaningfully higher than your expected tax rate later.

- FHSA: deduction today and tax-free qualifying first-home withdrawal later. Great when you qualify and want to buy a first home.

The cleanest mental model: TFSA is flexibility, RRSP is retirement tax planning, FHSA is first-home down-payment tax leverage.

Start here: the account order

- Take any employer RRSP match first. If your employer matches contributions, that match is part of your compensation. Capture it before optimizing the rest.

- Use FHSA first if you are eligible and want a first home. It can give you a deduction and a tax-free qualifying withdrawal, which is hard to beat for a down payment.

- Use TFSA next when flexibility matters. Emergency savings, uncertain plans, short-to-medium goals, career changes, moving, and early investing all fit well here.

- Use RRSP when the tax deduction is valuable. This usually means higher income, a clear retirement goal, or a year where reducing taxable income has an obvious benefit.

- Once one account is full, use the next best account for the goal. The order can change as your income, home plans, family situation, and contribution room change.

If you want to buy a first home

For an eligible first-time buyer, the FHSA usually deserves the first dollars because it combines the best part of the RRSP and the best part of the TFSA for one specific purpose. You may get a deduction when contributing, and if you use the money for a qualifying first-home withdrawal, the withdrawal can be tax-free.

- Use FHSA first if you are eligible, expect to buy within the FHSA window, and can leave the money invested or saved for the down payment.

- Use TFSA after FHSA for extra down-payment savings, closing costs, moving costs, furniture, or flexibility if the purchase date is uncertain.

- Use RRSP selectively if your income is high, you want the deduction, or you are considering the Home Buyers' Plan and understand repayment rules.

Related: read FHSA Explained and Should You Buy a Home in Canada? before treating the account as the only home-buying decision.

If you are new to Canada

A TFSA is often the easiest account to understand first because it is flexible and does not turn withdrawals into taxable income. That matters when your first Canadian years involve moving costs, job changes, emergency savings, immigration paperwork, furniture, family support, or uncertain income.

- Start with TFSA if you are building a cash buffer or learning Canadian investing.

- Add FHSA if you qualify as a first-time home buyer and home ownership is a real goal.

- Use RRSP carefully until your income is stable enough that the deduction is actually valuable.

Related: SIN, CRA, Bank Account, Phone Plan: First Admin Steps After Arriving in Canada.

If your income is low or moderate

A TFSA often wins at low or moderate income because you may not get much value from an RRSP deduction. If your tax rate is low today, saving the RRSP room for later can be useful. TFSA withdrawals also do not create taxable income, which keeps the account simple.

- Use TFSA first for emergency savings, early investing, and goals where you might need the money.

- Use FHSA first instead if the first-home goal is clear and you are eligible.

- Wait on extra RRSP contributions if you expect your income to be higher later and there is no employer match today.

If your income is high

At higher income, an RRSP can become powerful because the deduction can save tax at a higher marginal rate. The strategy works best when you invest the refund or use it intentionally, not when the refund disappears into random spending.

- Use RRSP earlier if you are in a high tax bracket and retirement saving is the goal.

- Still use FHSA first if you are eligible and buying a first home is likely.

- Use TFSA too for flexibility, tax-free growth, and money you may want before retirement.

If you have kids or benefit-tested income

RRSP contributions can reduce taxable income, which may affect some income-tested benefits and credits. This can make RRSPs more attractive for some families than the tax bracket alone suggests. TFSA withdrawals, by contrast, do not show up as taxable income.

- RRSP can help when lowering net income improves benefit calculations or reduces tax pressure.

- TFSA can help when you want savings that can be withdrawn later without adding taxable income.

- FHSA still wins for a first home if eligibility and home plans line up.

If you need emergency money

Emergency money should not be locked inside a strategy you are afraid to touch. A TFSA is usually the best registered account for emergency funds because withdrawals are flexible and the room generally returns the next calendar year. Keep emergency money in cash or low-risk savings, not volatile investments you may need to sell during a bad month.

- Use TFSA for emergency savings if you have TFSA room and want tax-free interest.

- Avoid RRSP for emergency money because withdrawals are taxable and room is generally not restored.

- Avoid FHSA for emergencies because it is built for a qualifying first-home withdrawal, not random cash needs.

If you are self-employed

Self-employed income can swing from year to year. That makes account order more strategic. A TFSA gives flexibility during uneven months. An RRSP can be useful in strong income years. An FHSA is still attractive if the home goal is real.

- Use TFSA for buffer money and flexible investing.

- Use RRSP in high-income years when a deduction is valuable.

- Use FHSA if you qualify and want a first home, especially in years where the deduction helps.

If retirement is the main goal

If you are not buying a first home and you already have emergency savings, the choice usually becomes TFSA versus RRSP. RRSP is stronger when your current tax rate is high and future withdrawals may be taxed lower. TFSA is stronger when you value flexibility, expect higher income later, or want tax-free withdrawals that do not add taxable income in retirement.

- Use RRSP first when current tax savings are strong and retirement is the real purpose.

- Use TFSA first when you want retirement savings that can also act as flexible life savings.

- Use both once contribution room and cash flow allow it. A blended strategy is common.

Common life-situation examples

- 22, first full-time job, unsure about plans: TFSA first, unless there is an employer RRSP match.

- 29, wants to buy a condo in a few years: FHSA first, then TFSA for extra down payment and closing costs.

- 35, high income, no home goal: RRSP and TFSA together, with RRSP getting more attention if the tax deduction is valuable.

- Newcomer building first Canadian safety net: TFSA for flexibility, then FHSA if eligible and planning to buy.

- Parent with strong income and benefit considerations: RRSP may be more attractive, while TFSA remains useful for flexible savings.

- Self-employed freelancer with uneven income: TFSA for buffer, RRSP in high-income years, FHSA if a first home is planned.

Mistakes to avoid

- Choosing by acronym instead of goal. The account should match the job: first home, retirement, or flexible savings.

- Spending the RRSP refund automatically. If the RRSP refund is part of the plan, put it to work.

- Using FHSA without checking eligibility. First-time home buyer rules matter.

- Overcontributing. TFSA, RRSP, and FHSA room are separate and penalties can apply when you exceed limits.

- Investing short-term money too aggressively. A house down payment needed soon should not be treated like a 30-year retirement portfolio.

A simple order that works for many Canadians

- Employer RRSP match, if available.

- FHSA, if eligible and first-home goal is real.

- TFSA for flexibility, emergency savings, and medium-term investing.

- RRSP for high-income tax planning and retirement.

- Non-registered investing once registered room is used or when the goal does not fit a registered account.

For deeper rules, read TFSA Explained, RRSP Explained, and FHSA Explained.

Related calculators

Use these to test contribution room, tax impact, and savings growth.

Related articles:

Page details

Author: Canooq Editorial

Updated: June 3, 2026

Cite this page: Canooq.ca, TFSA vs RRSP vs FHSA: Which Account Should You Use First?, https://canooq.ca/blog/tfsa-vs-rrsp-vs-fhsa-which-account-should-you-use-first

Canooq content is educational and may include affiliate or referral links. It is not financial, tax, legal, immigration, employment, mortgage, real estate, or healthcare advice. Verify official sources and provider terms before acting.