RRSP Explained: Contributions, Tax Refunds and Withdrawals in Canada

By Canooq Editorial

June 1, 2026

A beginner guide to RRSPs in Canada, including deductions, contribution room, refunds, taxable withdrawals, and when an RRSP makes sense.

QUICK START

An RRSP is mostly about tax timing.

Contributions can create a deduction today, while withdrawals are generally taxable later.

- Your RRSP deduction limit appears on your CRA notice of assessment.

- A refund is not free money. It is tax timing.

- RRSPs often make more sense when your tax rate is higher now than later.

Test a contribution

Use this article as a starting point, then check the linked official sources before acting.

What's on this page

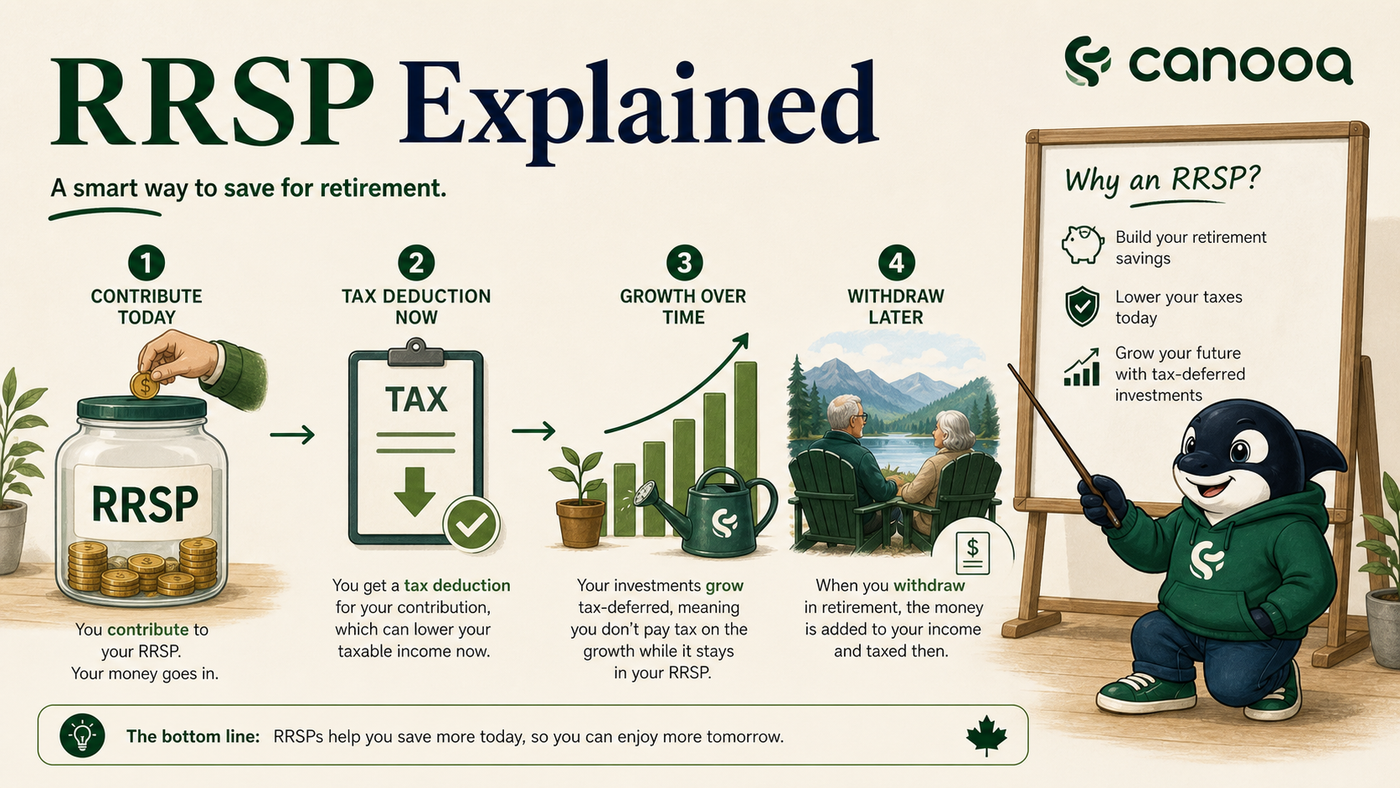

An RRSP can reduce taxable income today and defer tax until withdrawal. It works best when the deduction is valuable and retirement planning is the goal.

What an RRSP does

RRSP stands for Registered Retirement Savings Plan. It is a registered account designed mainly for retirement savings and tax deferral. You contribute within your RRSP deduction limit, investments can grow tax-deferred inside the plan, and withdrawals are generally taxable later.

The RRSP is not only an investment. It is the account wrapper. Inside it, you may hold cash, GICs, mutual funds, ETFs, stocks, bonds, and other qualified investments depending on the provider. The holdings should match how long the money can stay invested.

Who can use an RRSP

- You need available RRSP deduction room, usually created from prior earned income reported to the CRA.

- Your deduction limit appears on your notice of assessment and CRA account.

- RRSPs are often most useful when you expect your current tax rate to be higher than your tax rate when you withdraw.

Contribution limits, deadlines, and penalties

The 2026 RRSP dollar limit is $33,810, but your personal deduction room can be lower or higher depending on earned income, pension adjustments, unused room, and past activity. The annual formula is generally tied to 18% of earned income up to the dollar limit, with adjustments.

For a 2026 tax-year deduction, RRSP contributions made during 2026 and during the first 60 days of 2027 can generally be claimed, subject to your room. Excess contributions above your allowed cushion can trigger a 1% per month tax until corrected.

How the refund fits

An RRSP refund feels good, but it is not a separate bonus from the government. It usually means the contribution lowered taxable income for the year. If you spend the refund without a plan, the RRSP may still help, but you lose part of the compounding advantage.

Estimate an RRSP refund

Test how a contribution could affect taxes using a simplified estimator. Confirm official room before contributing.

Open calculatorWhen an RRSP makes sense

- You have a higher current income and expect a lower taxable income in retirement.

- Your employer matches RRSP or group retirement contributions.

- You want to save for retirement and can leave the money invested for years.

- You plan to reinvest the refund or use it for another high-priority goal.

When to be careful

- Your income is low and a deduction would not be very valuable right now.

- You may need the money soon, because regular withdrawals are taxable and can permanently use contribution room.

- You have high-interest debt or no emergency fund, which may be more urgent than extra retirement contributions.

RRSP or TFSA first?

The answer depends on income, employer plans, contribution room, flexibility needs, and future tax expectations. Someone in a high bracket may value an RRSP deduction. Someone with lower income, uncertain cash flow, or a medium-term goal may prefer TFSA flexibility.

RRSP vs TFSA vs FHSA

An RRSP is usually strongest for retirement tax planning. A TFSA is usually more flexible because eligible withdrawals are tax free and room returns the next calendar year. An FHSA can be stronger than both for an eligible first-home goal because it can combine a deduction with tax-free qualifying withdrawals.

If home ownership is the goal, read FHSA Explained before using RRSP room for a down payment plan.

Where Wealthsimple fits for an RRSP

Wealthsimple can be a useful RRSP provider if you want a simple digital account for long-term investing and recurring contributions. It works best when you already know your RRSP room and you want an easy place to hold diversified retirement investments. If you need complex tax planning, spousal RRSP advice, pension coordination, or withdrawal sequencing, get advice before relying on any app alone.

WealthsimpleWealthsimple offers a $25 referral bonus for the referee. Wealthsimple is a Canadian investing and money management platform.InvestingCashTFSARRSPFHSA

WealthsimpleWealthsimple offers a $25 referral bonus for the referee. Wealthsimple is a Canadian investing and money management platform.InvestingCashTFSARRSPFHSARelated articles:

Page details

Author: Canooq Editorial

Updated: June 3, 2026

Cite this page: Canooq.ca, RRSP Explained: Contributions, Tax Refunds and Withdrawals in Canada, https://canooq.ca/blog/rrsp-explained-canada

Canooq content is educational and may include affiliate or referral links. It is not financial, tax, legal, immigration, employment, mortgage, real estate, or healthcare advice. Verify official sources and provider terms before acting.